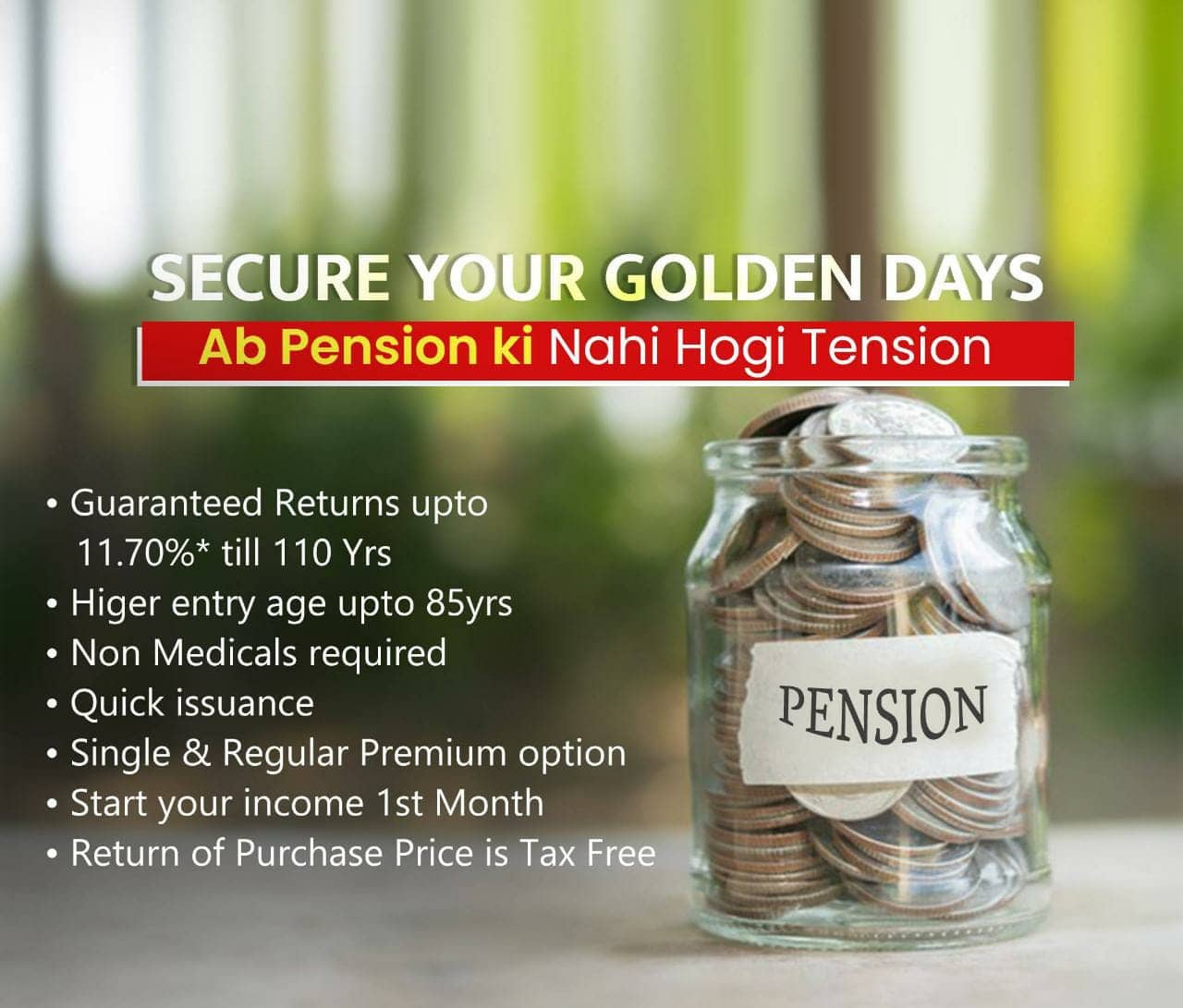

Retirement is much a reality as much as its planning a neglected activity. Retirement planning continues to be ignored by most individuals. There is a lot more to retirement than just resting on an armchair and playing with grandchildren. Retirement planning includes identifying various sources of income, estimating the expenses, implementing a savings program and managing assets.

A prerequisite for a comfortable retired life is detailed planning. Goals need to be define and investments to be made to make the best of the golden days.Retirement for some it could be turning to God, others would occupy themselves with a remunerative profession, while some would want to travel to make up for what has been missed during the earlier days. Whatever be the occupation, the expenses would continue ... the grocery bills, the house rents, the power charges, gifts for the younger ones, so on and so forth. So while expenses would continue, the primary source of income would the missing.

The retirement objectives are met with proper investments planning. A portion of investments in riskier instruments like the stock markets which gives higher returns, while a portion is safer havens like bank fixed deposits and gold which, inspite of its lower returns, protects the capital. The key to a healthy retirement is a well-planned retirement. And a retirement is well-planned when the planning begins with enough time at hand. There are many reasons why planning for retirement has to begin early :

1. Increased Life expectancy: With the advancement in medical science, the life span has increased as compared to the previous years. Longer life means a longer period post-retirement. Means, you will have to save more to meet those years of lower / no income.

2. Medical expenditure: Increasing age brings along with it increased medical expenditure. This does not include medical emergencies, but covers more visits to the doctor and the regular dose of medicines.

3. Medical emergencies: A medical emergency can often be a big drain at the savings. Although, medical insurances cover most of these expenses; yet sometimes the emergencies cost a lot more than the cover taken. A higher insurance cover means a higher premium, and gets still higher with rising age. With youngsters moving jobs at an increased frequency, they are not eligible for benefits like gratuity etc. Moreover, such benefits which are handed over at the time of quitting the job are considered as a bonus rather than remembering that their objective is retirement.

4. Inflation: As you need to worry about it you need to account for it as well. You need to take into account inflation while calculating your retirement corpus as well as your returns. The value of money diminishes with every passing day. Money saved today is much lower than its value tomorrow. These and there are handful of other reasons why retirement planning needs to start early, for every day comes with a price. If you have inherited a 2 Crore mansion from your rich uncle and plan to sell it, you need not worry to accumulate 1 Crore when you retire. But, if you need to plan your retirement, which you must, then take a look at how much you need to save every month, to become a multi-millionaire when you retire. We make the following assumptions to save an inflation-adjusted 1 Crore

Retirement age: 60 years

Average Annual inflation: 5%

Return on savings: 12%

Present age Required monthly saving:

• 25 years 5,975

• 30 years 8,702

• 35 years 12,938

• 40 years 19,875

• 45 years 32,295

Planning for retirement is a lifelong process. Whether you're just starting to invest or you're well into your working years, this checklist can serve as a starting point to help prepare you for this important financial goal.

Starting early and contributing as much as possible to employer-sponsored retirement plans and government funds may help you to potentially save more money. Why? Because longer the money sits untouched, the more it can potentially compound.

Another vital step: Determine an appropriate asset allocation -- how you divide your money among stocks, bonds, and cash -- for your portfolio. This should be based on your financial goals, tolerance for investment risk, and time horizon. Be aware that your asset allocation will need to be adjusted periodically in response to major market moves or life changes.

Once you're nearing retirement, it will also be necessary to craft a solid plan for distribution of your assets. For example, do you know one of the greatest risks that retirees face? The possibility of outliving their money.

Retirement Checklist:

1. Have you performed a comprehensive retirement needs calculation?

2. Are you contributing enough to potentially reach your financial goal within your desired time frame?

3. Is your asset allocation aligned with your retirement goal, risk tolerance, and time horizon?

4. Is your asset allocation properly spread out? A part to provide you with guaranteed returns, albeit moderate, and a part to provide a little higher returns. Please be very very careful investing in schemes where returns are abnormally high and much beyond market standards.

5. Do you review your retirement portfolio each year and rebalance your asset allocation if necessary?

6. Have you considered your health insurance options, (i.e., Mediclaim and/or employer-sponsored health insurance), out-of-pocket medical expenses, and other related health care costs? Maybe you would need to take up a second health insurance now, as after retirement your present employer will no longer cover you, and a new health insurer would not want to take up a new (high) risk.

7. Have you reviewed all your financial and legal documents to make sure beneficiaries are up-to-date?